Life Insurance Paid Out in Bitcoin

More than 100 million Americans either need to obtain life insurance or increase the amount of their coverage. No one likes to think about the topic, but life insurance is a crucial part of financial planning, and any savvy investor should make sure their loved ones will be protected. Life insurance is a crucial part of planning for your long-term future, no matter your net worth.

With Bitcoin’s rise in price to above $100,000 for the first time, it gained even more notoriety and is an increasingly popular investment. It is not only so-called “crypto millionaires” holding Bitcoin, but also everyday investors who want a diversified portfolio. The need for financial and estate planning around Bitcoin and other digital assets has grown, but current offerings have not yet caught up with demand.

There is a clear need for insurance products denominated in Bitcoin for investors who want to hold BTC for the long run, and who also want to ensure that their loved ones are taken care of.

What is Whole Life Insurance?

(Investopedia)

Life insurance is fairly straightforward - you make payments - “premiums” - to a life insurance company for an insurance policy. The policy’s value is based on your age, health, and actuarial calculations made by the insurance company. When you die, the life insurance company pays out the value of the policy to your heirs.

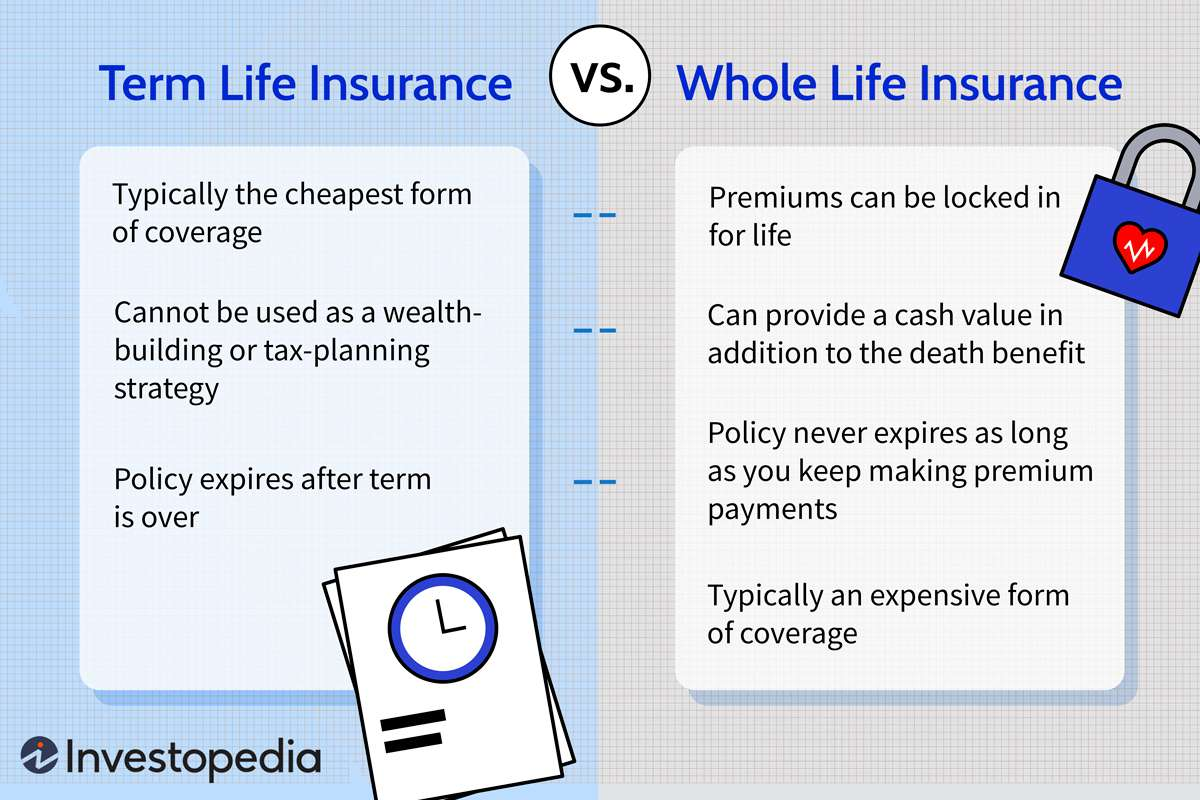

Whole life policies offer a guaranteed payout no matter when the insured person dies, as opposed to “term life” policies that will only pay out during the fixed term of the policy. For example, a “term life” policy may cover you from ages 30-50, and then expire if you live past 50, requiring you to purchase a new policy for a new term if you want continuing coverage.

Whole life policies also have a “cash value,” which is the amount of money you can get out of the policy if you choose to cancel it. It is based upon the premiums you have paid in, and the amount of time they have had a chance to grow, as the cash value compounds with time. Those gains are tax-free. You can also borrow money against the cash value, without having to pay any capital gains taxes.

Whole life insurance policies have three main benefits when compared to term life policies - a guaranteed payout, tax-advantaged growth, and tax-free liquidity via policy loans.

Previously, crypto investors had no way to use their Bitcoin for whole life policies, which allows them to keep crypto exposure while knowing their heirs will benefit.

Who is Meanwhile?

Meanwhile is the first and only life insurance company denominated in Bitcoin, which means that you pay premiums exclusively in Bitcoin and the benefits are paid out in Bitcoin. It was founded in 2022 by CEO Zac Townsend and CTO Max Gasner, both of whom have founded successful startups. Zac is a McKinsey alum who sold a banking API business to Silicon Valley Bank, while Max was on the founding team of a startup that was sold to Salesforce. The company has raised over $20 million from notable investors such as OpenAI CEO Sam Altman, and Google’s Gradient Ventures.

Meanwhile has been writing life insurance policies since 2023, has thousands of registered users, and custodies tens of millions of dollars worth of Bitcoin.

How does it work?

Meanwhile’s life insurance policies are open to 18-65 year olds in the U.S. and Canada. It will be open to U.K. residents shortly, with more international jurisdictions to come in 2025.

The applicant/policyholder fills out an online application with medical underwriting done digitally. The ideal policy size to request will differ based on your own financial picture.

You will receive an offer, usually within 24 hours, with the death benefit determined by Meanwhile based on an actuarial assessment.

You pay premiums for 10 years, or there is the option to transfer your payments ahead of schedule via their Premium Pre-Funding Rider. Once those ten payments are made, the policy is fully funded.

The minimum premium amount is 1 BTC, so the annual payment would be 0.1 BTC. The maximum face amount of a policy is 50 BTC.

Once the first payment is made, your beneficiaries are guaranteed to receive a full payout when you die, even if it happens within the first ten years.

Why buy life insurance with Meanwhile?

First and foremost, Meanwhile is the only company offering life insurance policies entirely denominated in Bitcoin. Not only do you and your heirs benefit if the price of Bitcoin rises, but the amount of Bitcoin in your policy also grows over time. Policy holdings are guaranteed to compound 2% per year, and that growth is tax-free.

After the second year of your policy, you can borrow up to 90% of the policy’s current “surrender value” tax-free. The surrender value is the current value of the loan based on the premiums paid in and the time elapsed. There is no capital gains tax on any appreciation in the value of your Bitcoin, as it is technically a loan against the value of your policy and gets a stepped up cost basis. It can be sold immediately at cost and you would not owe any capital gains tax. If any loan is still outstanding at the time of your death, it will be netted against the death benefit.

This tax-free liquidity against your Bitcoin holdings can be of significant value to investors. For example, let's say you pay BTC premiums into your policy with a cost basis of $100,000. After two years, the price of BTC rises to $200,000. You can borrow BTC against the value of your policy and sell it immediately at cost, meaning you would not owe capital gains on the $100,000 of appreciation that occurred while the BTC was in the policy. If you had simply held that BTC, you'd be on the hook for ~$15,000 (depending on tax bracket) in capital gains taxes. If BTC rises higher, or if you borrow more, it doesn’t matter - you will never have to pay capital gains taxes on anything you borrow.

Bitcoin is a complicated asset, and can get particularly tricky if you are hoping to leave it to your heirs. If your family does not have access to your wallet, passwords and keys, the value of your entire digital asset portfolio could be lost if you die unexpectedly. A Bitcoin life insurance policy ensures that your heirs will always receive the face value of the policy upon your death, with no confusion over keys and wallets. Meanwhile custodies Bitcoin with Anchorage Digital, so customers can be secure in the knowledge that their assets are safe.

Meanwhile makes money the same way standard life insurance providers make money - by investing their capital, making loans and charging interest. They make conservative investments to ensure they can meet the 2% guaranteed returns, and have yet to see any credit losses. Meanwhile has a solid capital base and maintains a minimum solvency ratio of 150%. They have an independent board, an investment committee, risk management controls and are regulated by the Bermuda Monetary Authority, a global leader in insurance regulation. Ultimately, Meanwhile is just like any other life insurance company, except that they deal only in Bitcoin.

“As a dad and bitcoiner to two young kids, I have been waiting for a product offering like Meanwhile since they were born. Meanwhile is the perfect product market fit for our family and our estate planning needs. The onboarding process was seamless and the customer service was excellent.” - Actual Meanwhile customer

A one-of-a-kind product

Everyone with dependents should have life insurance to make sure their loved ones are protected. Life insurance denominated in Bitcoin is the ideal product for anyone that thinks Bitcoin will appreciate in price over the long-term and want to tax-efficiently tap into that value during their lifetime. Meanwhile is the only company that offers this kind of product and also ensures that their customers’ digital assets will be protected and transferred to their heirs.